Q4 2025 Investment Commentary

Introduction - Book Review - Portfolio Review - Feature - Factsheet

Summary

Introduction – Annual Review

We look back on the last year and reflect on our progress towards our long-term goals.Books That Influenced Our Thinking in 2025

We review two books that helped us understand China’s growing global dominance.Portfolio Review

A review of key portfolio changes during the quarter, including new investments, trims, and exits.Performance Review

An overview of the companies that most influenced portfolio performance this quarter — both positively and negatively.Feature – VersaBank

We review a non-traditional bank that is at an inflection point, expanding its point-of-sale financing solution into the U.S.Factsheet

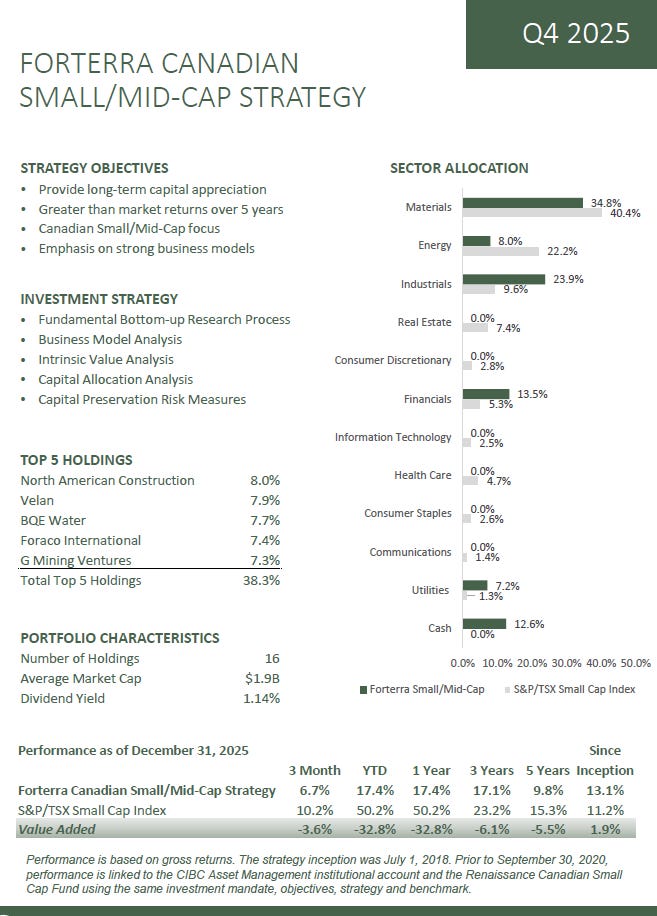

A concise snapshot of the portfolio, including sector exposure, top holdings, and historical performance.

Introduction

Annual Review

This time of year is an opportunity to step back and reflect on our performance, our progress toward our longer-term goals, and what the past year tells us about our investment process.

We know we will not outperform every year, and 2025 presented several challenges. Below, I review our results relative to both our benchmark and our peers. I also examine how our decisions during the year added to or detracted from performance, and whether we remain on track toward our long-term objective of compounding capital.

Compounding Performance

Our primary objective is to compound capital over time. We aim to double capital over a five- to seven-year period, which requires annualized returns of approximately 10–15%.

While a steady path would be ideal, we know that any five-year period is likely to include one or two difficult years, which is why we frame our goal over a longer window.

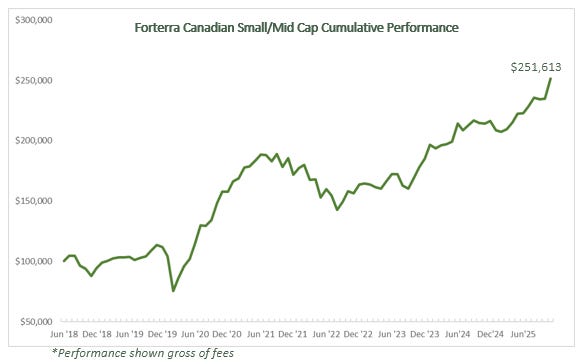

The portfolio’s absolute return of 17.4% in 2025 contributed positively to this objective. Since inception, the strategy has delivered an annualized return of 13.1%. An initial investment of $100,000 on July 1, 2018, would have grown to more than $250,000 today.

Measured against our core objective of compounding capital over time, we remain confident that we are on track to meet this objective.

Performance vs. Benchmark

We underperformed our benchmark, the S&P/TSX Small Cap Index. The index delivered an exceptional year, which returned 50.2%. That outcome was driven by its growing concentration in gold and silver companies, which approached 35% of the index by year-end. The Materials sector rose 136.9% in 2025, largely reflecting the strength in precious metals.

None of the more than 30 industry peers we track were able to outperform the benchmark in 2025. This is not a year in which we would expect to outperform.

The benchmark remains a useful comparison over the medium to long term, but it can be misleading over shorter periods when performance is dominated by a single theme or sector. A year ago, we were ahead of the benchmark across all measured time periods, and by a wide margin over five years and since inception. One extreme year has materially lifted the benchmark’s long-term numbers.

Since inception, now seven and a half years ago, we remain ahead of the benchmark. Over time, as returns normalize and become less concentrated in a single sector, we remain confident in our ability to outperform.

Performance vs. Peers

We underperformed our peer group in 2025. We track approximately 30 Canadian small-cap strategies that we consider representative peers. Many peers in the market are hedge funds or institutional managers that do not publicly report performance, so this group is indicative rather than exhaustive.

Our portfolio is intentionally concentrated, holding between 16 and 18 companies over the past year, compared with 40 or more positions for most peers. In a year with a few setbacks, most notably Colabor and Mattr, that concentration had a more pronounced impact on our results than it did for more diversified portfolios.

Among the strategies that outperformed, common characteristics included very broad diversification, often 80 or more holdings, sector exposure that closely resembled the index, and, in many cases, a tilt toward higher market-capitalization companies. We will never build a portfolio with 80 holdings, mirror index sector weights, or focus on mid-caps simply for the sake of size. Our edge lies in identifying smaller companies early, before they are widely recognized.

We are disappointed with our relative performance this year. Some of the factors that drove peer outperformance are not ones we are willing to adopt. Portfolio concentration hurt us in 2025, but it has been a meaningful contributor to strong performance in prior years. We know we will not outperform every year, and this was one of those years.

Performance vs. Ourselves

Each year, we also evaluate what we call the Static Portfolio. This measures the performance of the portfolio as it stood on January 1, assuming no trading occurred throughout the year. The goal is to assess whether our trading activity added or detracted value.

Over time, I’ve found that a two-year comparison is often more informative, given our longer investment horizon. This year, I was particularly interested in the results. Much of the year was spent trimming strong performers such as G Mining Ventures and K92 Mining, while adding to positions like Mattr as they declined.

Looking at both one- and two-year static portfolios, our active results were in line with the static outcomes. In both cases, G Mining Ventures and K92 Mining would have exceeded 10% position sizes, with G Mining Ventures reaching nearly 20% of the portfolio. If we cap position sizes at 10%, roughly where we limit them in practice, our active management outperformed the static portfolios across both time frames.

In reality, we would never allow two highly correlated gold companies to represent 32% of the portfolio. Managing that risk is critical, and we are pleased that trimming did not come at the expense of long-term performance. Capital was redeployed into new ideas and selectively added to core positions at appropriate times. We are satisfied that our actions are adding value through time. We aim to continue to strike the right balance between letting our investments compound over the long-term and course correcting when necessary.

I want to thank our clients for placing your trust in us. My capital is invested alongside yours, and I aim to continue to compound capital over the long-term.

-Robert

Books That Influenced Our Thinking in 2025

As the global economy continues to shift from a largely unipolar, U.S.-centric structure toward a more multipolar world, it has become increasingly important to understand the role China plays today — and the trajectory it is on. To that end, two books stood out to us in 2025: Apple in China: The Capture of the World’s Greatest Company by Patrick McGee and Breakneck: China’s Quest to Engineer the Future by Dan Wang.

Both books place China squarely at the centre of the narrative, but from very different perspectives. McGee tells the story through the lens of Apple, the world’s most iconic consumer technology company. Wang approaches it through China’s long-standing identity as a nation of engineers and builders. Together, they paint a compelling and, at times, uncomfortable picture of China’s evolution into a manufacturing and technological superpower.

Importantly, both books dismantle the outdated notion that China’s primary competitive advantage lies in low-cost labour and low-quality production. That may have been closer to the truth fifteen or twenty years ago, but it is no longer an accurate framework. Instead, they highlight China’s willingness to think in decades, its capacity to align policy with capital investment, and the advantages conferred by an autocratic system that can pursue long-term objectives with remarkable consistency.

A 2015 Beijing policy document titled Made in China 2025 captures this mindset succinctly: “Without a strong manufacturing industry, there will be no country and no nation.” China’s ambitions are clear — dominance in manufacturing and technology and increasing self-reliance across critical industries.

Apple in China: The Capture of the World’s Greatest Company — Patrick McGee

At its core, Apple in China is the story of how Apple came to outsource its manufacturing, and how that decision ultimately led it into deep dependence on China. While the subject matter may not sound like a page-turner, McGee’s writing makes it exactly that.

The book traces Apple’s manufacturing journey from the U.S. to Asia. First in Japan — where Apple’s demanding design standards further elevated already capable suppliers — to Taiwan, and eventually to mainland China. In China, generous government subsidies and an unmatched willingness to build infrastructure at scale made the country an irresistible destination for Apple’s supply chain.

A central figure in the story is Foxconn, the Taiwanese contract manufacturer that helped Apple establish its footprint in China. Rather than limiting itself to low-margin final assembly, Foxconn aggressively pursued vertical integration. That strategy required an enormous workforce, which in turn led to close coordination with Chinese regional governments. Entire cities were built around Apple’s production needs, complete with dormitories, cafeterias, transit systems, and entertainment complexes.

As Apple’s scale grew, so did its bargaining power. Margins were increasingly pushed lower for suppliers like Foxconn, as volumes surged. Foxconn accepted this trade-off because it was playing a much longer game. By manufacturing Apple’s most complex products, it was effectively training its workforce to operate at the highest level of global hardware engineering.

Today, McGee argues, Apple has few viable alternatives. No other country can match China’s combination of scale, speed, and technical capability at Apple’s required cost structure. While Apple has announced plans to diversify production into India and elsewhere, the book suggests it could take more than a decade before any meaningful volume is shifted. In that sense, Apple has been “captured.”

Viewed through Apple’s experience, the book offers a sobering reality check for investors. It has implications not just for consumer electronics, but for any industry involving advanced manufacturing where China already has a foothold — from smartphones to electric vehicles. Companies attempting to compete with Chinese manufacturers face a daunting challenge.

A striking example is Xiaomi. Founded only in 2010 and often referred to as the “Apple of China,” Xiaomi is now a global smartphone leader. In 2021, it did something Apple has yet to accomplish: it launched an electric vehicle. A quick search for a “Xiaomi factory tour,” or Marques Brownlee’s recent video Driving Xiaomi’s Electric Car: Are We Cooked?, offers a revealing look at just how fast this transition is happening — particularly as many legacy automakers continue to struggle to produce compelling EVs.

Breakneck: China’s Quest to Engineer the Future — Dan Wang

If Apple in China explains how the world’s most valuable company became embedded in China’s manufacturing ecosystem, Breakneck helps explain why that ecosystem exists in the first place.

Dan Wang’s book is less about any single company and more about a cultural and institutional mindset. It examines China through the lens of its engineers, builders, and system designers - people who are focused on solving problems at scale. Wang argues that China’s rise is best understood not as a story of imitation, but as one of relentless iteration, execution, and learning-by-doing.

A recurring theme throughout the book is that China excels at what Wang calls “engineering-driven growth.” Rather than relying on breakthrough innovation alone, China focuses on making things work, then making them better, faster, and cheaper. This approach rewards speed, adaptability, and pragmatism — traits that are deeply embedded in China’s industrial culture.

Wang contrasts this with Western economies that increasingly prioritize finance, regulation, and services over manufacturing. In China, engineers still sit close to power. Technical competence is respected, and large-scale projects are seen as nation-building exercises rather than political liabilities. This helps explain China’s willingness to invest aggressively in infrastructure, automation, logistics, and manufacturing capacity, even when near-term returns are uncertain.

From an investment perspective, Breakneck provides critical context for understanding why Chinese companies can scale so quickly once they find product-market fit. It also explains why China has been able to close the gap, and in some cases surpass global competitors, in industries such as renewable energy, electric vehicles, batteries, telecommunications equipment, and advanced manufacturing.

The book is particularly useful in framing China’s long-term self-reliance goals. Rather than seeking dominance for its own sake, Wang argues that China’s priority is resilience: ensuring it can build, supply, and maintain critical systems without external dependency. This lens helps explain policy decisions that might otherwise appear inefficient or heavy-handed when viewed through a purely market-driven framework.

Taken together with Apple in China, Breakneck reinforces a central takeaway: China’s competitive advantage is not a single technology or company, but a system. It is a system that aligns labour, capital, policy, and infrastructure toward clear objectives — and one that improves through repetition and scale.

For investors, this has meaningful implications. It challenges assumptions about where durable competitive advantages will emerge, how long they can persist, and which regions are best positioned to compound industrial capabilities over time. In a world that is becoming less globalized and more fragmented, understanding these dynamics is no longer optional.

Portfolio Review

The Forterra Canadian Small/Mid-Cap portfolio returned 6.7% gross of fees in Q4 2025, compared to the S&P/TSX Small Cap Index’s 10.2% gain.

The Materials sector drove index performance, rising 22% and now representing over 40% of the index on strength in gold, silver, and copper. While the portfolio has exposure to these commodities, we remain underweight relative to the index.

It was another busy quarter. We exited two positions, initiated two new ones, and both trimmed and added to several core holdings.

We sold our position in Colabor Group in October following a third-quarter update that announced the replacement of the CEO and a requirement from lenders that the company raise at least $15 million to recapitalize its balance sheet. Colabor was already the smallest position in the portfolio and given the increased probability that equity holders would be wiped out as debt holders assumed control, we exited the position to preserve what value remained. Colabor entered creditor protection in early January after failing to raise the required capital in December, which led to a further collapse in the share price.

Our process emphasizes risk management through position sizing and ongoing assessment of fundamental business risks. In Colabor’s case, those fundamentals deteriorated rapidly. Our discipline—keeping the position small, avoiding additional capital deployment once the news turned negative, and exiting promptly when the thesis broke—limited but did not prevent the loss.

This experience offers important lessons. While we believe the situation was exacerbated by poor leadership decisions and an ineffective board, that does not change the fact that our thesis was wrong. The greater mistake would be failing to reflect on it. This is a difficult and uncomfortable part of investing, and one that is rarely discussed. Mistakes are inevitable, but learning from them is essential. As investors who view this work as a lifelong apprenticeship, this reflection is how we improve our craft.

We trimmed our position in G Mining Ventures as the share price continued to move higher, managing its size within the portfolio.

We initiated the position in G Mining Ventures less than three years ago at an average cost of $3.40, and it ended 2025 at $41.49. The outcomes of both Colabor and G Mining Ventures demonstrate that our investment process can produce large losses and exponential gains. These results are also reminders that we are not as foolish as our worst investment may imply, nor are we as brilliant as our best investment might have us believe.

With proceeds from trimming G Mining Ventures, we initiated two new positions: Elemental Royalty, a gold-focused streaming and royalty company, and Rio2 Limited, a mining company nearing production at its Fenix Gold project in Chile. We also added to Magna Mining as our conviction in the company’s long-term prospects increased.

We continue to see compelling opportunities in mining despite the sector’s recent revaluation. The portfolio’s growing exposure to gold and copper focuses on companies with distinct paths to value creation beyond commodity price appreciation alone.

In November, we exited Mattr following a cautious third-quarter outlook. After touring the company’s new Xerxes facility in South Carolina and meeting with management, we concluded that the risk profile had changed materially. Our original thesis centred on the strength of the Shawflex business, once considered the company’s crown jewel. What was previously a source of stability has become a source of risk.

Rising trade tensions and global tariff uncertainty have increased operational risk, particularly while CUSMA remains unresolved. We see a meaningful chance that this uncertainty persists through most of 2026, with rolling extensions making long-term capital allocation decisions more difficult.

While Mattr could recover and re-rate, we also see risk of further deterioration before improving. Management has acknowledged the difficulty in forecasting this environment and has suspended share buybacks to prioritize debt reduction. This reflects fewer available options and a necessary focus on balance sheet sustainability,

We invest through uncertainty when we can reasonably assess how it may resolve. In this case, we do not see clarity until trade agreements are finalized. We will continue to monitor Mattr closely, but we remain on the sidelines.

Performance Review

Gold and silver equities outperformed in Q4 as precious metals momentum continued. The largest contributor to performance was G Mining Ventures, which rose 50% during the quarter. Despite its strong run, we continue to see upside as the company advances toward production at its Oko West project.

K92 Mining was also a strong contributor, gaining 35%, while Rio2 Limited, the newest gold position in the portfolio, rose 65% from our initial purchase in early October.

Velan rose 19.6%, after announcing valve orders exceeding $20 million for the Pickering Nuclear Generation Station refurbishment. Subsequent to quarter end, the Velan family agreed to sell their controlling position in the company at a significant discount to market value to Birch Hill, a private equity firm. We view the discount as a measure of the family’s single-minded focus on selling the company quickly and Birch Hill’s shrewd negotiating. We continue to believe that the shares are undervalued – as does Birch Hill – given that they just underwrote a long-term investment where they expect to make a multiple of their capital over the next decade.

BQE Water rose 18.3% after securing a 20-year contract with the British Columbia government for the operation and maintenance of the Britannia Mine Water Treatment Plant, reinforcing the company’s differentiated capabilities. VersaBank gained 20.6% after reporting positive earnings and providing a favourable outlook for 2026. See our Feature section for more on our investment thesis.

The largest detractor was Colabor, which declined 70% before we exited in October. The company mismanaged an acquisition intended to drive growth, taking on excessive debt without sufficient cash flow to support operations. Lender demands for equity issuance further pressured the share price.

Mattr also detracted, falling 37.5% before we sold in November on tariff uncertainty. goeasy declined 24.3% following a mixed earnings release with elevated credit provisioning that raised concerns about future credit losses. In December, the newly appointed CEO stepped down for health reasons, adding further uncertainty. We continue to view goeasy as a strong long-term business, while recognizing that sentiment-driven volatility can be pronounced in the short term.

Feature - VersaBank

Company Overview

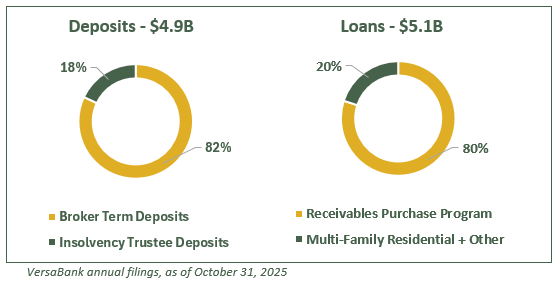

VersaBank is unlike any other Schedule I chartered bank in Canada. Its core business is providing point-of-sale funding to finance companies through its Receivables Purchase Program (RPP). The company has successfully scaled this model in Canada over the past 15 years and has recently launched the same RPP solution in the U.S., a market that is more than ten times the size of Canada.

Like a traditional bank, VersaBank earns the majority of its income from the spread between interest earned on loans and interest paid on deposits. That is largely where the similarities end. VersaBank’s deposit base is primarily composed of deposit brokers and wealth managers seeking competitive term deposits (GICs with terms of up to five years) from an insured Schedule I bank. VersaBank has longstanding relationships in this channel and a track record of offering competitive rates.

The company also operates a specialized, technology-enabled deposit solution for insolvency professionals, who are required to hold trustee funds with a Schedule I bank. These deposits tend to be less rate-sensitive and have become an increasingly important source of funding. Combined, these two deposit channels grew at an average rate of approximately 17% in 2025.

On the asset side, the loan portfolio is dominated by the Receivables Purchase Program. VersaBank partners with finance companies that originate point-of-sale (POS) loans for large consumer purchases such as HVAC systems, roofing, and water heaters. The finance company originates the loan and benefits from quick, efficient access to funding from VersaBank—often faster and less complex than alternatives such as securitization or warehouse facilities.

VersaBank also maintains a portfolio of multi-family residential mortgages and loans, which are predominantly CMHC-insured and carry low credit risk. While this has been a stable line of business for many years, management expects future loan growth to be driven primarily by the RPP in both Canada and the U.S.

History

The company was founded in 1979 as Pacific & Western Bank of Canada, a provincially licensed trust company based in Saskatchewan. In 1993, President and CEO David Taylor, along with a group of investors, acquired the bank. In 2002, it was granted a Schedule I bank charter, with its head office established in London, Ontario.

VersaBank went public in August 2013. At the time, the business was primarily focused on commercial real estate and multi-family lending, alongside the early framework of what would later evolve into the Receivables Purchase Program. Its deposit strategy—raising funds through deposit brokers via competitive term deposits—was already in place, and in 2013 the bank began diversifying deposits by developing solutions for insolvency trustees.

At the time of its IPO, VersaBank employed 83 people across London, Waterloo, and Saskatoon. It also operated a wholly owned subsidiary, Versabanq Innovations Inc., which held its proprietary deposit-management software. Following an amalgamation in 2016, the company was renamed VersaBank.

Competitive Advantages

Risk Management Technology

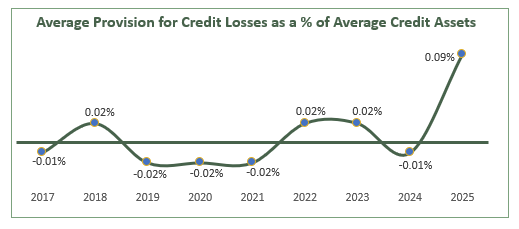

VersaBank’s RPP structure is central to its competitive advantage. For each partner, the bank carefully defines underwriting criteria and uses historical loss experience to determine appropriate holdback reserves. This structure allows VersaBank to rapidly purchase receivables, freeing up capital for originators and enabling them to scale more efficiently.

Loans that become more than 90 days past due can be put back to the originator, materially reducing VersaBank’s exposure to credit losses. This mechanism helps explain the bank’s historically low loss experience. While the RPP model is complex and initially took time for us to fully understand, we believe it represents a meaningful and underappreciated advantage.

Innovation and Niche Focus

VersaBank has a long history of identifying niche opportunities where it can apply its existing capabilities. The RPP solution, refined over 15 years in Canada, is now being adapted to the U.S. market. The company is also enhancing the platform using AI to enable near-instantaneous funding decisions, which could expand partner relationships and increase wallet share.

On the deposit side, VersaBank developed proprietary technology tailored to insolvency professionals, creating a lower-cost and stickier funding source. The company has also pursued innovation through digital assets, developing Real Bank Deposit Tokens (RBDTs) and VersaVault, a secure digital asset custody solution.

This entrepreneurial mindset is unusual in banking. VersaBank operates more like a founder-led fintech than a traditional Schedule I bank—and that cultural difference is part of its edge.

Investment Case

Our investment thesis rests on two primary pillars: U.S. growth and operating leverage.

U.S. Growth

The U.S. point-of-sale financing market is estimated to be more than ten times the size of Canada’s. VersaBank has already established partnerships, since entering the market earlier in 2025, with many more potential relationships ahead. While competition is greater and alternatives such as securitization are more readily available, VersaBank’s speed and efficiency provide a compelling complementary funding solution.

In addition to RPP growth, VersaBank has begun purchasing senior (A-tranche) securitizations, which are highly capital-efficient and accretive given current net interest margins. We expect approximately $1 billion in U.S. credit asset growth in 2026, split between RPP and securitizations, with customized RPP solutions accounting for a greater share over time.

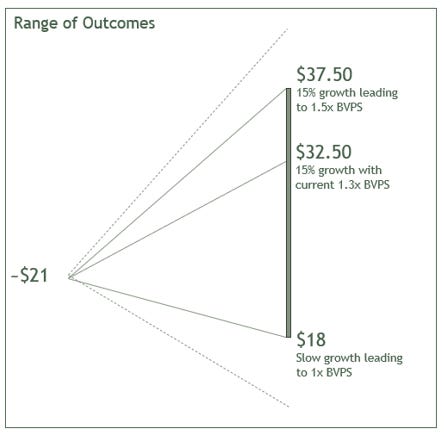

We believe this growth can drive book value per share from approximately $16.50 today to roughly $25 over the next three years.

Operating Leverage

With just 130 full-time employees and no branches or consumer-facing infrastructure, VersaBank is highly scalable. As a condition of receiving its U.S. bank charter, the company is divesting its small cybersecurity division, which we estimate could reduce annual operating expenses by $8–9 million.

Although the recent corporate redomiciling to the U.S. introduces incremental costs, we expect net operating expenses to decline overall. Improved efficiency should drive returns on equity meaningfully higher. We believe 15%+ ROE is achievable within three years (and 20%+ within five years), from ~10% ROE today. This trajectory would support a strong valuation multiple expansion.

Optionality

VersaBank has several sources of upside not included in our base case:

Stronger Growth in the US – VersaBank could experience greater market penetration and signup new partners at a faster pace.

RPP Innovation – VersaBank is in the process of improving the speed of funding in the RPP offering using artificial intelligence, which has the potential to increase its appeal and widen the potential partnership opportunities.

Digital Asset Market Penetration – There is a greater openness to digital asset solutions today, and VersaBank has a leadership position with multiple solutions in the piloting stage. VersaBank’s Real Bank Deposit Tokens (RBDTs) function like a stablecoin but are backed by a bank and pay interest. VersaBank recently announced that it has signed an agreement with Stablecorp to serve as the custodian of their QCAD stablecoin. This agreement is an endorsement from a company whose investors include Coinbase, Circle and DeFi Technologies.

Risks

Partner Risks – VersaBank works with a relatively small number of POS partners for its RPP solution. This counterparty concentration poses a risk if there is a departure or a failure. VersaBank’s partners on the deposit side are also somewhat concentrated and losing key channel partners could be disruptive.

Execution Risk – VersaBank is known for building technology-focused solutions. New products need to be properly structured and tested before going live with clients. There also needs to be a strong business case for new solutions.

Regulatory Risk – VersaBank operates in a highly regulated federal banking environment. Compliance is necessary, along with anticipating and adapting to new policy changes.

Macroeconomic Risks – Employment levels and the health of the consumer influence both demand for point-of-sale financing and loan performance, particularly in a sharp downturn.

Valuation

VersaBank currently trades at approximately 1.3x book value and 12.5x 2026E earnings, reflecting growing investor confidence following the successful expansion of its U.S. business having achieved its US$290 million U.S. loan and securitization target.

We track a detailed financial model to understand the moving parts, but we believe a long-term perspective is more informative than focusing on near-term quarterly results. If VersaBank can sustain or modestly expand its net interest margin and achieve operating leverage as it scales in the U.S., we expect continued growth in book value per share and a rising return on equity.

Over the next three years, we estimate book value per share could grow at roughly 15% annually, driven primarily by U.S. asset growth and improving efficiency. Under this scenario, and assuming no valuation multiple expansion, we estimate fair value of approximately $32.50 per share. If the market assigns a modest premium multiple of 1.5x book value, consistent with financial companies growing in the mid-teens with improving ROEs, shares could approach $37.50 by 2028.

We take a longer-term view and consider where the business could be over the next three to five years. Our 15% growth assumption is above VersaBank’s historical book value growth rate of closer to 8%, reflecting what we see as a structural inflection point driven by U.S. expansion. The pace of growth is inherently uncertain, but even if this trajectory is achieved over five years (closer to 10% annual growth), we still see an attractive return opportunity.

Importantly, our base case does not fully reflect the company’s embedded optionality. If U.S. growth accelerates, RPP innovation expands the addressable market, or digital asset initiatives gain traction, the value of the business could be materially higher. In an upside scenario, we believe the stock could potentially double over the next three years, making the risk-reward profile compelling.

Final Thoughts

VersaBank is a rare example of a truly differentiated bank. It lacks branches, does not serve retail customers, and partners primarily with private financial intermediaries. In many respects, it resembles a fintech—driven by innovation, efficiency, and niche focus—while still making money the old-fashioned way, through a positive net interest margin.

Companies without clear comparables are often misunderstood and mispriced. VersaBank is no exception. It took time for us to fully understand the business model and its risk controls, but that effort has been rewarded. The company is far better positioned today than it was just two years ago, with a clearer growth runway, improving economics, and meaningful operating leverage ahead.

We believe VersaBank is approaching an inflection point. If management continues to execute without credit missteps, the combination of growth, improving returns, and increasing visibility should speak for itself.