Q3 2025 Investment Commentary

Introduction - Market Commentary - Portfolio Review - Feature - Factsheet

Summary

Introduction – Five Years of Reflection

We look back on the past five years — the challenges of building something new and the rewards that have come with it.Market Commentary – Gradually, Then Suddenly

We explore how change often builds slowly before accelerating rapidly, and how this dynamic relates to the signs emerging in today’s markets.Portfolio Review

A review of key portfolio changes during the quarter, including new investments, trims, and exits.Performance Review

An overview of the companies that most influenced portfolio performance this quarter — both positively and negatively.Feature – Firan Technology Group

We highlight an aerospace and defence company well-positioned to benefit from strong industry tailwinds and to continue compounding value over time.Factsheet

A concise snapshot of the portfolio, including sector exposure, top holdings, and historical performance.

Introduction

The Long Game: Reflections on the First Five Years

It has now been five years since I left the bank—an experience that, at the time, came with uncertainty and imperfect timing. The world was in the midst of the pandemic, and it wasn’t the easiest moment to start a new venture. But in hindsight, that period of disruption created space to pause, reflect, and think differently about what I wanted to build.

Leaving behind the familiarity of a large institution is never simple. There are the practical concerns—losing the security of a steady paycheck—and the personal ones, like letting go of the identity tied to your role. There’s also the quiet loss of community: the daily exchange of ideas, the mentorship, and the energy that comes from working alongside talented colleagues.

Still, there were parts of that world I was ready to leave behind: the pressure to put profits ahead of people; products designed for shareholders before clients; and the layers of bureaucracy and politics that too often rewarded conformity over merit.

Entrepreneurship brings a different kind of pressure. The safety nets are gone, and every outcome, good or bad, rests on your shoulders. Social media can make it look glamorous, but the reality is more humbling. The work is demanding and, at times, isolating. You wear every hat, and there’s no “out-of-office” mode.

Yet the rewards have far outweighed the risks. I have the privilege of working directly with clients, helping them reach their goals and navigate an increasingly complex world. I get to spend my time doing what I love: researching, analysing, and thinking critically about companies. And I’ve found a renewed sense of community through mentors, clients, and peers who challenge and inspire me.

Five years later, I’m proud of the journey. It hasn’t been easy, but it’s been worth every risk. The work is challenging, purposeful, and deeply rewarding. I’m exactly where I’m meant to be.

Thank you to my clients and supporters for your trust.

-Robert

Market Commentary

Gradually, Then Suddenly

“How did you go bankrupt?” Hemingway’s character is asked in The Sun Also Rises.

“Two ways,” he replies. “Gradually, then suddenly.”

That phrase captures something profound about how change unfolds in complex systems, whether biological, social, or financial. Shifts that appear slow and manageable often mask deep structural imbalances building beneath the surface. And when those systems reach a critical point, the change that follows feels abrupt, even shocking, though it was long in the making.

Today’s market environment feels increasingly defined by these “gradual” dynamics. The mounting sovereign debt, eroding faith in paper currencies, and the gradual return of gold to central bank vaults. Each trend alone may appear benign; together, they could suggest a world inching toward a new equilibrium that could arrive “suddenly.”

Understanding Sudden Change

1. Complexity and Phase Transitions

In physics and systems theory, phase transitions occur when gradual changes reach a threshold and trigger a qualitative shift like water freezing, sandpiles collapsing, or ecosystems flipping states. Markets, too, are complex adaptive systems: capital flows, policy decisions, and investor psychology build tension over time. The “sudden” moments, the crises, crashes, or paradigm shifts, are not random shocks but the natural release of accumulated stress.

2. The Tipping Point

Sociologist and acclaimed author Malcolm Gladwell popularized the term, but the underlying concept is older: social and economic systems often hold steady until enough actors change behaviour, at which point the shift becomes self-reinforcing. Investor sentiment, technological adoption, or policy confidence can all follow this pattern. The first few central banks buying gold are ignored; when a dozen more follow, it begins to shape market expectations. The same holds for investor rotations away from U.S. mega-caps or diversification away from the dollar. A few isolated moves can suddenly become a flood.

3. The Minsky Moment

Economist Hyman Minsky (1919–1996) spent his career studying how stability breeds instability. His insight was simple yet powerful: prolonged periods of calm encourage risk-taking, leverage, and complacency. As financial actors move from “hedge finance” (safe borrowing) to “speculative” and then “Ponzi” finance (reliance on ever-rising asset prices), the system becomes fragile. A Minsky Moment occurs when confidence breaks, typically triggered by a seemingly small event, and asset values reset abruptly.

Examples abound: the 1998 LTCM collapse, the 2008 mortgage crisis, even the 2020 liquidity shock. What unites them is the illusion of safety preceding the storm. Today, one could argue that sovereign debt markets, AI-driven valuations, or geopolitical complacency may be nurturing their own Minsky-like dynamics.

The Gradual Trends Taking Shape Today

The Debt, the Dollar, and the Drift Toward Gold

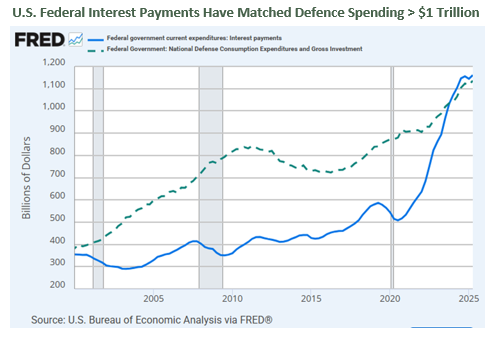

The gradual rise of U.S. government debt is perhaps the most visible “slow burn.” For decades, deficits have grown with little consequence. No inflation spiral, no funding crisis, no apparent limit to investor demand. Yet debt-to-GDP now exceeds 120%, and interest payments rival defence spending. Markets have adjusted gradually to this new normal, but the fiscal math remains unsustainable without higher growth, higher taxes, or inflation.

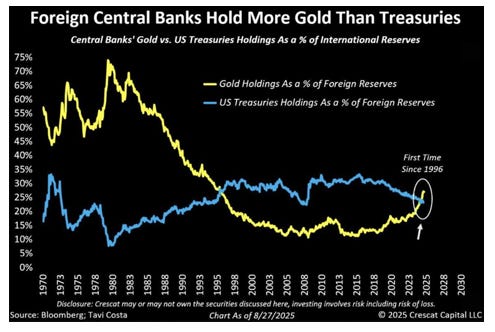

Simultaneously, confidence in the U.S. dollar’s permanence as the world’s reserve currency is eroding. No single event marks the transition, it’s visible instead in gradual diversification: China and India settling trades in local currencies, and the steady buildup of gold reserves across emerging markets. Central banks bought more gold in 2022–2024 than in any comparable three-year stretch since the 1960s.

Individually, these actions are unremarkable; collectively, they signal hedging against the long-term viability of the dollar-centric order. Like Hemingway’s character, the erosion of monetary dominance may happen “gradually”, until it happens all at once.

The Magnificent Seven and the AI Investment Boom

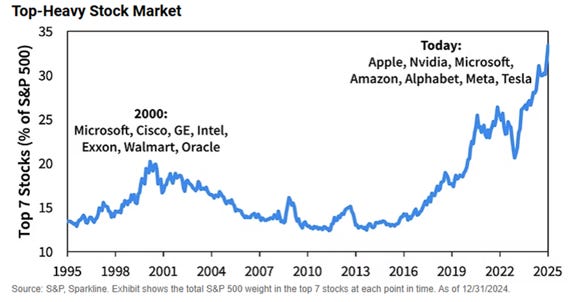

A second area of slow accumulation lies in market concentration and capital allocation. The “Magnificent Seven” stocks -Apple, Microsoft, Amazon, Alphabet, Meta, Tesla, and Nvidia - now account for nearly 35% of the S&P 500’s market capitalization. Such dominance evokes the “Nifty Fifty” of the early 1970s, a group of blue chips once thought invincible until inflation and recession exposed their vulnerability.

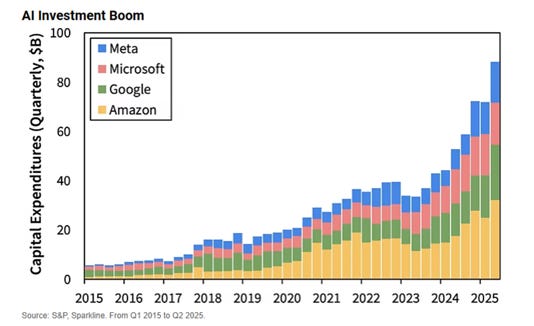

Meanwhile, corporate spending on artificial intelligence has exploded. The optimism may prove justified, but capital cycles are prone to over-building. The parallels to the 1990s telecom buildout or 19th-century railway mania are striking. Vast infrastructure investment preceding a painful shakeout. AI may follow the same pattern: gradual enthusiasm morphing into sudden repricing when expectations collide with financial reality. How does one begin to measure the return on the enormous capital that is being spent today? The race may make sense for a few players in a “winner-take-most” outcome that we often see in technology, but what happens to the rest of the players and most of the capital?

Implications for Investors

The challenge is recognizing when “gradual” transitions near the breaking point. Investors should not assume that long-running trends be it fiscal expansion, dollar dominance, or AI-led growth, can persist indefinitely without adjustment. Nonlinear shifts often emerge from familiar places.

Valuation Discipline means stress-testing assumptions to evaluate the true range of outcomes. It also means focusing on cash flows and hard asset values and away from relative metrics like prices/sales ratios which can “suddenly” become less relevant.

Diversification beyond dominant investment themes, whether that is the Magnificent Seven, AI spending or the flight to gold. Real diversification requires investments that are not concentrated in a theme and are not correlated to one another.

Patience and scepticism remain virtues in markets that reward momentum. Trends can persist, but as complacency builds it is often punished harshly.

As in complexity theory, stability and fragility coexist. The most dangerous moment often feels the safest. “The water is warm – come on in” said the frog to all who will listen.

Living in the “Gradual”

We may well be living through the “gradual” phase of several major transitions -fiscal, technological, and monetary. None appear urgent until they are. The goal for investors is not to predict the exact “suddenly,” but to recognize the structures that make it inevitable.

Economist Rudi Dornbusch put it best:

“Things take longer to happen than you think they will, and then they happen faster than you thought they could.”

At Forterra, we are treading carefully, focused on where we see compelling value and looking for companies that have true measures of resilience.

In markets, as in history, change rarely announces itself. It creeps, accumulates, and then, all at once, it’s here.

Portfolio Review

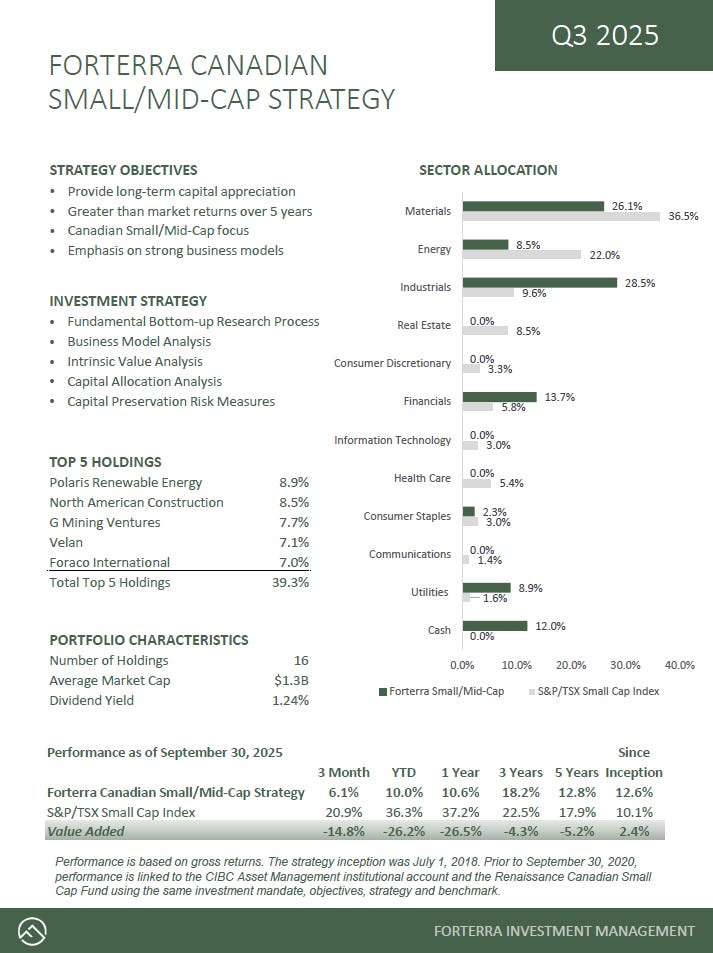

During the third quarter of 2025, the Forterra Canadian Small/Mid-Cap portfolio returned 6.1% gross of fees, underperforming the S&P/TSX Small Cap Index, which gained a remarkable 20.9%. The index’s strength was largely driven by its heavy weighting in gold and silver companies, which rose on average more than 40% during the quarter. The S&P/STX Composite Index advanced 12.5%, continuing to deliver the strongest returns across the developed markets both for the quarter and year-to-date.

Market volatility continued to create opportunities to trim and add to portfolio positions. During the period, we exited two holdings, initiated one new position, and added to several high-conviction names.

We sold our position in Sylogist following another disappointing quarter of results and guidance. We first invested in Sylogist several years ago, building the position in the $6 per share range as the company began repositioning towards a SaaS-based business model. While we recognized this transition would take time, management repeatedly overpromised and underdelivered, forcing multiple revisions to its outlook. With credibility eroding and our revised outlook implying limited upside, we concluded the stock was close to fair value near $8 per share and exited the position.

Since our sale, shareholder OneMove Capital has called for a special meeting to overhaul the board. While activism could catalyze change, we see no easy fixes and view it as a potential distraction. Management is capable, but the company’s growth narrative needs rethinking. The stock has declined over 25% since our exit; for now, we remain on the sidelines pending more clarity on strategic direction.

We also trimmed and eventually sold Andean Precious Metals as it quickly exceeded our fair value range. We had acquired shares in March and April around $1.65, which we viewed as an absolute bargain. As silver prices surged, Andean’s shares rallied sharply, eventually surpassing $5 in August. We reduced the position to manage risk and ultimately exited entirely. Momentum traders had driven the stock far beyond our valuation range, leaving little upside outside of further commodity price increases. While our timing is never perfect, the decision was grounded in risk management and valuation discipline. Andean ended the quarter at $8.30, lifted further by rising gold and silver prices.

We trimmed the Trisura Group position around $44 to align its portfolio weight with its upside potential. The stock has traded between $30 and $45 over the past four years; we previously added in the low $30s. With Trisura now re-establishing a pattern of strong operating results, we expect it to break out of this range and continue to view it as a core holding.

We added to North American Construction Group following a weak quarter, viewing most challenges as temporary and largely beyond management’s control. Having seen this team execute through past cycles, we used the pullback to increase our position with confidence in the company’s long-term outlook. We also added to Foraco International, as the market continues to overlook its strong margins, new contract wins, and disciplined execution. We view Foraco as a highly asymmetric way to gain diversified mining exposure, without relying on any single commodity, region, or operator.

Similarly, we added to Atlas Engineered Products as cyclical headwinds tested investor sentiment. While the stock weakened, we see a company using this period to strengthen its competitive position. When construction activity rebounds, we believe Atlas will emerge as a stronger market leader. Buying when others are fearful is never easy, but our research-driven, long-term approach gives us conviction and helps mitigate the risk of being wrong.

We initiated a new position in Magna Mining, a Sudbury-based copper and nickel producer. Through a series of acquisitions, Magna has transformed itself into a copper-producing company with a flexible, low-cost mining plan. The team, many of whom were instrumental in building FNX Mining, has a proven track record of operational success. With a solid balance sheet and permitted, past-producing assets ready to restart, we believe Magna is well-positioned to become a leading low-cost mid-tier base metals producer.

Finally, we added to Firan Technology Group, which we see as well-positioned to benefit from robust demand in both the aerospace and defence sectors. (See our Feature Section for more on Firan.)

Performance Review

Precious metals continued to shine in the third quarter, propelling gold and silver companies to new heights. The largest contributor to performance was once again, Andean Precious Metals, which rose another 78% before we sold the position in August.

G Mining Ventures, the gold miner with a producing mine in Brazil and a development project in Guyana was up 55% over the period. We continue to see value in the company as they get closer to bringing their Oko West project into production. Foraco International also contributed to performance in the quarter, up 13% amid renewed optimism in the mining sector.

Polaris Renewable Energy rose 13% as it moved closer to bringing online several projects with strong expected returns over the next 12-18 months.

The largest detractor over the period was Colabor Group, as shares slid 36% amid multiple setbacks: softer growth, a repriced contract, a delayed acquisition closing, a cyberattack and a temporary forbearance agreement with lenders. After the quarter-end, the board chair passed away suddenly, the CEO was dismissed and several board members resigned. Despite the ongoing sell-off, we exited the position given our view that lenders -not shareholders- are likely to be prioritized in any turnaround effort. The company’s situation has changed materially over the past six months. It was the smallest position in the portfolio as we viewed the risk as elevated, but manageable before all these events unfolded, minimizing the impact to the portfolio.

We will reassess to see if there is an opportunity for equity investors to benefit from the turnaround, but in the meantime, we will observe from the sidelines. It pains us to take losses like this, but we realize it comes with the territory. It is a reminder to risk-manage positions, remain highly sceptical and to take losses early if things are going off track fundamentally.

North American Construction Group also detracted value, falling 9.3% on a weaker quarter. As noted earlier, we added to the position, viewing the pullback as a buying opportunity. We remain positive on the company’s long-term prospects and have created value in the past by taking advantage of similar periods of volatility.

Feature - Firan Technology Group

Firan Technology Group (FTG) is a Toronto-based manufacturer of electronic products for the aerospace and defence industries. Its FTG Circuits division builds printed circuit boards, while FTG Aerospace manufactures illuminated cockpit panels and electronic assemblies. The company focuses on niche markets where their customers qualify products based on technical specifications and consistent quality.

FTG operates 11 facilities across North America and Asia, including one facility under development in India. Approximately 60% of revenue comes from the aerospace industry and 40% from defence. They serve an impressive roster of clients, many of which it has partnered with for decades.

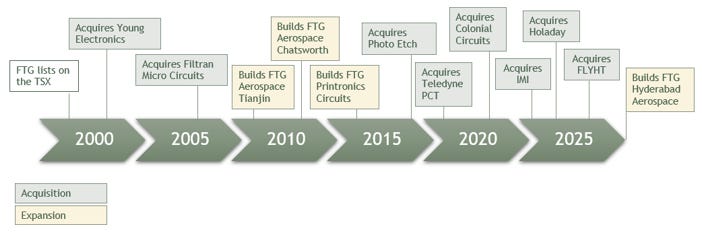

History

FTG traces its roots back to 1983, when it was founded as Helix Circuits. The company rebranded and listed on the Toronto Stock Exchange in 2003, marking the beginning of its current strategic focus on aerospace and defence. Since then, FTG has expanded through both acquisitions and organic growth, opening new facilities to meet rising demand. Over time, its global footprint, production capacity, and ability to deliver higher-specification products have all grown significantly.

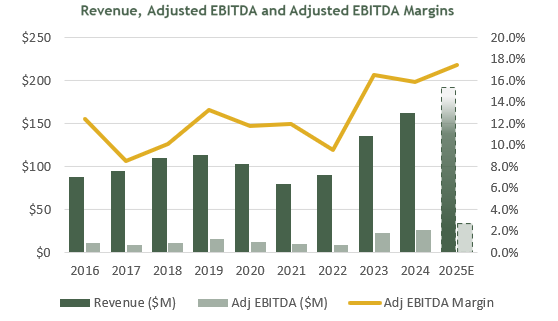

FTG has delivered robust growth in recent years, with revenue increasing from $90 million in 2022 to $162 million in 2024 -a 34% compound annual growth rate (CAGR) driven by both organic expansion and acquisitions. Despite a pullback during the COVID years, FTG’s 10-year revenue CAGR remains around 9%, while EBITDA has grown closer to 15% over that period.

Looking ahead, we expect ~18% revenue growth in 2025 and 10–12% in 2026, with earnings growing roughly 15% annually. The balance sheet remains conservative, with less than 1x leverage, providing ample financial flexibility.

COVID and Supply Chain Challenges

FTG faced meaningful headwinds during the COVID period, when global supply chains were severely disrupted. While FTG managed its own supply chain relatively well, many large aerospace programs it supplied were slowed by their own production issues. Boeing also dealt with quality issues on their 737 MAX program creating further disruptions.

This period of inconsistent results and lower profitability pressured the company’s market valuation. Now that these challenges are behind it, FTG has demonstrated renewed revenue growth and margin expansion through operating leverage. We believe that historical trading multiples during the COVID period are not a good reference point when assessing FTG’s future value.

Competitive Advantages

Qualification and Certification Barriers

Aerospace and defence are highly regulated industries with significant barriers to entry. It can take years for suppliers to qualify for major programs, as both OEMs and Tier-1 suppliers require rigorous certification. Over two decades, FTG has built a strong reputation for reliability—a quality not easily replicated.

A Tier-1 avionics supplier to both Airbus and Boeing recently chose to move its business from a competitor to FTG, a process that took several years. This new contract should add approximately $5 million in annual revenue beginning in 2026, demonstrating FTG’s growing reputation and market share gains.

Technology Leadership

FTG continues to evolve alongside its customers, manufacturing increasingly complex circuit boards and aerospace components. This close collaboration fosters innovation and strengthens customer relationships, further enhancing FTG’s competitive position.

Manufacturing Flexibility

With production facilities in Canada, the U.S., and China, FTG can serve major clients efficiently while optimizing production for cost, labour availability, and technical expertise. For example, production of cockpit assemblies for COMAC’s C919 aircraft is currently being migrated from Toronto to Tianjin, China. This flexibility is a strategic advantage amid rising global trade barriers. While some cost adjustments occur, these have largely been absorbed by customers.

Investment Case

Annuity-Like Programs – Most FTG products are sold into large aerospace and defence programs that can run for decades. Because qualifying new suppliers is difficult, these relationships are extremely sticky, roughly 80% of FTG’s work is sole-sourced. We believe this re-occurring and durable revenue base remains underappreciated by the market.

Strong Cyclical Tailwinds – The aerospace industry has seen steady growth coming out of the weakness brought on by the covid-induced supply chain issues. Both Boeing and Airbus have order backlogs that are over a decade long based on today’s run-rate of production. Even in an economic slowdown, we expect any cancellations to be replaced by other customers moving up the queue, supporting a long, steady growth cycle.

The defence sector also remains robust amid the war in Ukraine and rising geopolitical tensions in the Middle East and Asia. We expect NATO members to continue ramping up defence spending, extending the cycle and making it less correlated to broader economic trends.

Operational and Capital Allocation Track Record – FTG has a long and successful history of growth through expansion and acquisition. Its growth has been thoughtful, and the capital allocation record shows that there has been discipline. FTG managed to complete acquisitions despite a low valuation and limited access to capital, demonstrating disciplined execution. The company has also shown sound judgment in its buy-versus-build decisions when pursuing growth opportunities. Their previous expansions have been successful, and we expect that the expansion into India will also prove successful in the long-term.

We’ve also observed a culture of continuous improvement, from optimizing plant layouts to sharing technical expertise across sites. Recent examples include shifting production between facilities to drive long-term efficiency and plans to insource some manufacturing from the FLYHT acquisition. These initiatives require effort and time, but demonstrate FTG’s operational discipline and long-term mindset.

Optionality

Potential Acquisition

With a strong balance sheet, FTG has room for another acquisition. Management has expressed interest in expanding into Europe, potentially to deepen its Airbus relationships and tap into rising defence spending across the continent. While our base case does not rely on additional M&A, we believe it is likely over time.

After-Market Sales Opportunities

FTG’s recent FLYHT acquisition introduces products now coming to market after years of development. While our growth assumptions are conservative, aftermarket sales—given their higher margins—represent potential upside to earnings if adoption accelerates.

New Program Wins – FTG has been qualified on new programs over the last 12-18 months that have yet to see any orders placed. While it is hard to predict the timing and the magnitude of orders, we expect that FTG will continue to get qualified and win content on new and existing programs. Our investment case assumes market-like organic growth on their existing base of business – all new programs would represent upside to our forecast.

Early Progress in India

FTG’s new Hyderabad facility is in development. Although we have modest near-term expectations, India’s ambitions to expand its aerospace and defence industries could create early opportunities. Any traction here would provide additional upside to our investment case.

Risks

Operational Execution: FTG’s reputation is built on reliability. Any quality issues could materially impact customer relationships and future contracts.

Customer Concentration: While the client base has diversified, losing a top customer would remain significant. This risk should decline as FTG grows.

CEO Succession: CEO Brad Bourne has led FTG for over two decades. Recognizing succession planning as a key priority, the board and management have strengthened the leadership team by hiring a new CFO and division heads for Aerospace and Circuits, each having potential of eventually assuming the top role.

Tariffs and Trade Barriers: FTG has not been materially affected by tariffs to date, but remains exposed to potential changes in CUSMA or other trade agreements.

Valuation

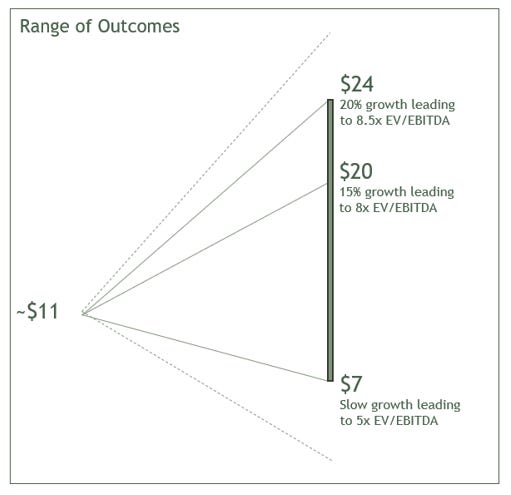

FTG’s current valuation remains attractive at <7.5x 2026E EV/EBITDA and a ~10% 2026E free cash flow yield (excluding growth capex), for a business growing at double-digit rates.

We take a long-term approach and have a three-year target price of $20 per share, based on:

8x 2029E EV/EBITDA

Our 5- Year DCF model (12% discount rate, 3% terminal growth rate)

~15% EBITDA CAGR (2026–2029)

~15% ROIC

This forecast assumes 10–12% organic revenue growth and modest expansion-driven contributions, with no M&A or outsized program wins. Upside to $24 per share could materialize if an accretive acquisition occurs or growth exceeds expectations. Conversely, even with slower growth, the downside appears limited, potentially to around $7 per share if multiples compress.

Overall, we see FTG as an asymmetric opportunity: steady progress with attractive long-term upside and limited downside. We don’t expect quick catalysts, but rather consistent compounding over several years. Even if it takes four years instead of three to reach our $20 target, we will be satisfied shareholders.

Pushback on Valuation

Some investors believe FTG’s re-rating opportunity has passed, given its ~100% share price gain in the 12 months ending September 30, 2025. While understandable, we think this view overlooks key context.

FTG’s historical valuation was depressed by pandemic-era supply chain issues that caused inconsistent earnings. The company is now larger, more stable, and better understood by investors. With a market cap above $250 million and improved liquidity, FTG is attracting a broader shareholder base.

Our valuation assumes only a modest multiple expansion—from ~7.5x to 8x EV/EBITDA over the forecast period. This seems reasonable for a company expected to deliver consistent, double-digit growth. Notably, FTG’s closest peer, TTM Technologies, trades around 15x 2026E EV/EBITDA. While FTG could justify a higher multiple, our thesis does not rely on one, it’s attractive even under conservative assumptions.

Final Thoughts

As noted in prior commentaries, we look for asymmetric opportunities, investments that can double in value over a three- to five-year horizon. We believe FTG fits that profile.

Our investment thesis is informed by direct discussions with CEO Brad Bourne, senior leadership, and board members, as well as on-site visits to FTG’s Toronto Circuits and Aerospace facilities earlier this year. We’ve also conducted extensive competitive analysis, supply chain research, and end-market evaluations.

We don’t expect explosive near-term growth, but we do see FTG as a long-term compounder, a company steadily building value for patient investors over the next 3–5 years.

This reads like a masterclass in patience and perspective. The reflection on gradual versus sudden change is important. How market shifts always seem obvious only after they happen. The discipline in trimming strength, adding on weakness, and keeping conviction through the noise shows the difficult craft of true investing, I would agree.