Q1 2026 Investment Commentary

Introduction - Market Commentary - Portfolio Review - Feature - Factsheet

Summary

Introduction – The Power of a Good Story

Every investment thesis is a story. The hard part is knowing when yours has gradually changed.

Market Commentary - The Price of Passage

From oil to fertilizer to food: how a narrow strait became the world's most consequential bottleneck.Portfolio Review

A review of key portfolio changes during the quarter, including new investments, trims, and exits.Performance Review

An overview of the companies that most influenced portfolio performance this quarter — both positively and negatively.Feature – BQE Water

The funnel is filling, not emptying — an update on BQE Water and why we are staying the course.Factsheet

A concise snapshot of the portfolio, including sector exposure, top holdings, and historical performance.

Introduction

The Power of a Good Story

We all like a good story. A book. A film. Something shared over dinner that stays with you long after the table is cleared. Stories are how we make sense of the world and how we connect with the people in it.

Investing, for all its numbers and spreadsheets, is no different. Stories are everywhere in this business, and they are not incidental. They are often the thing driving the decision.

When we meet with a CEO, they are telling us a story about a company’s past and its outlook for the future. It might be a turnaround story, an innovation story, a consolidation story, or a tale about hidden assets the market has not yet discovered. As investors, we are building our own version of that story, the investment thesis, the reason we own what we own. Sometimes it aligns with the prevailing market view. Sometimes it runs against it. But it is always a story.

Stories can carry risk, and we see two danger areas in particular.

The first is being seduced by someone else’s story. A well-constructed investment pitch can be a masterclass in selective emphasis: it leads with the opportunity, addresses the objections quickly, and ends with a picture of what the upside looks like. Add a sense of urgency — this opportunity won’t last long — and the pressure to act before you have done sufficient work can be significant. This is the oldest technique in sales, and it is used in investing for the same reason it is used everywhere else: it works. Our research process is deliberately slow and methodical, not always working to our advantage, but as a consistent check against moving too fast on a compelling story.

The second danger is less discussed, because the storyteller is you.

Once an investment is made, it is entirely natural for the thesis to evolve as circumstances change. In our world, when this happens unintentionally it is called thesis drift. It tends to be gradual, and it tends to be invisible. A company you bought for three clear reasons has seen one of those reasons slowly erode. A competitive advantage has narrowed. A management change has altered the leadership within the business. And yet, when you consult your memory, you find a way to accommodate these changes — you always expected some competition, you knew the founder would eventually step back. You have not changed your mind. You have simply updated the story, in real time, without noticing.

This is why we journal. This is why we maintain a written investment thesis rather than relying on memory, which is a poor and partial historian. We also use a thesis tracker, a living record of the key assumptions behind each investment, and the specific indicators we watch to assess whether those assumptions are holding. The goal is not rigidity. An investment thesis can evolve. But that evolution should be deliberate and the assumptions underlying a changing risk profile should be recorded and underwritten. What we want to avoid is arriving somewhere we did not intend to go, holding a position we would not have built under the current set of facts.

Most investors have a process for evaluating other people’s narratives. Fewer have one for scrutinising their own. We highlight this part of our process to demonstrate how we try to mitigate these behavioural biases. Our process is not perfect, but we are sharing this because we believe transparency about how we think is as important as transparency about what we own. Our trusted clients deserve to know not just the story, but how carefully we are watching it.

-Robert

Market Commentary

The year began on solid footing. Markets were pricing in multiple U.S. rate cuts, earnings expectations were constructive, and broad indices sat near all-time highs. Then, the mood shifted quickly as the risk of a war with Iran escalated and energy prices began moving sharply higher.

The Price of Passage

The Strait of Hormuz is 34 kilometres wide at its narrowest point. For decades, roughly a fifth of the world’s seaborne oil and liquefied natural gas has reliably passed through it each day. Since late February 2026, that has changed. The US-Israel military campaign against Iran effectively closed the strait, and the consequences are now working their way through every layer of the global economy.

Second Order Effects

Brent crude, which started the year around $73 per barrel, has surged past $100 and briefly touched $126 — its highest level in four years. The International Energy Agency has called it the largest supply disruption in the history of the oil market. What receives less attention, but may prove equally consequential, is the impacts to the fertilizer industry. About a third of the world’s basic fertilizers pass through the Strait of Hormuz, and Gulf producers stand among the world’s largest producers of urea and ammonia. Fertilizer prices jumped 20 to 30% in the first month of the conflict, arriving at the worst possible moment, the beginning of the Northern Hemisphere planting season. Food prices are a lagging indicator of fertilizer costs. We are watching the fuse burn.

Inflation’s Oldest Story

Energy-driven inflation is not new. The 1973 OPEC embargo, the 1979–80 oil shocks, and the post-COVID energy surge of 2021–22 all followed the same pattern: an energy shock transmits into transport costs, into industrial inputs, into food, and eventually into consumer prices broadly. Central banks then face an uncomfortable choice — tighten into a slowing economy, or let inflation run.

The mechanism is the same today. Higher oil prices raise fuel costs for trucks, ships, and aircraft. Freight surcharges rise, squeezing retailers and consumers alike. Airlines face margin compression. At the household level, real wages erode when energy inflates faster than incomes. For companies with energy-intensive or logistics-dependent operations, the pressure on margins — and ultimately on earnings multiples — is real and accumulating.

Our Portfolio in This Moment

No portfolio is fully insulated from a shock of this magnitude, and we would not pretend otherwise. What we can say is that ours was not built for any single scenario. It was constructed from the bottom up to be resilient across an entire cycle — and we shift it gradually to where we see value in the market, not in reaction to the news of the day.

We hold meaningful exposure to gold equities, which have historically offered both capital preservation and operating leverage in inflationary environments. We also own businesses with high-quality earnings streams — companies with pricing power, low capital intensity, and the ability to protect their margins even as input costs rise.

The situation in the Strait of Hormuz remains unresolved, and the ripple effects into food, freight, and consumer affordability are still building. We are watching closely. Our discipline, as always, is to stay balanced, trust the quality of what we own, and remain patient for the opportunities that dislocations tend to create.

Portfolio Review

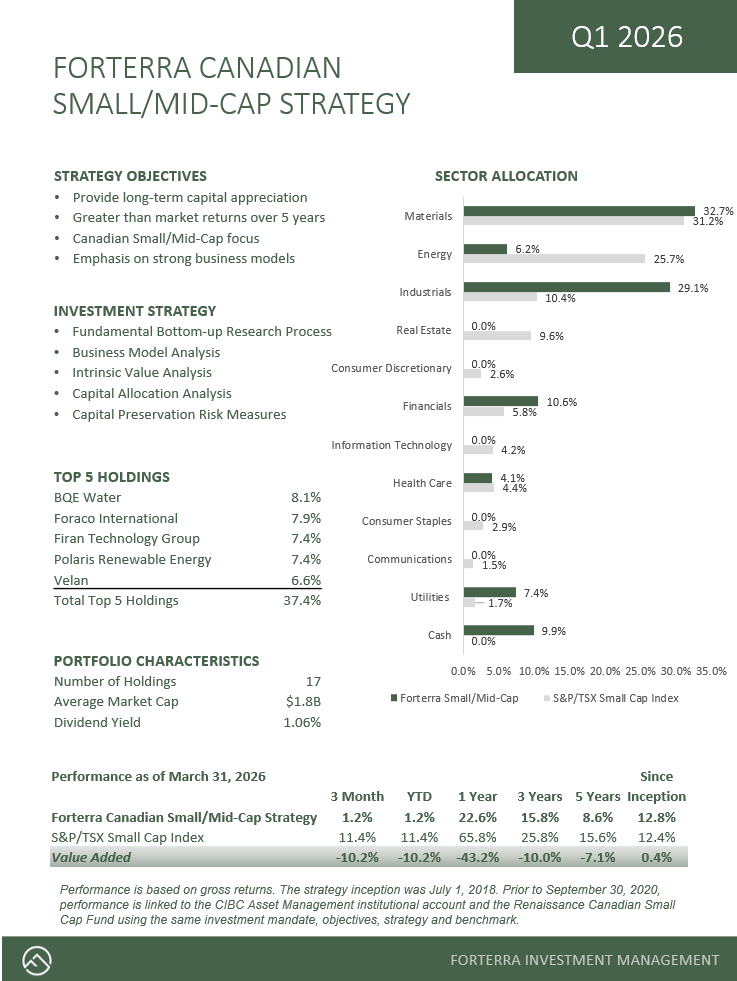

The Forterra Canadian Small/Mid-Cap portfolio returned 1.2% gross of fees in Q1 2026, against an 11.4% gain for the S&P/TSX Small Cap Index.

The gap is largely explained by one word: oil. The Energy sector surged over 30% as war in Iran roiled global oil markets. With Energy representing roughly 28% of the index, that move carried significant index weight. We have no direct exposure to oil and gas producers — a deliberate and long-standing decision. Smaller producers face structural headwinds: limited resource diversification, higher costs of capital, and few of the scale advantages enjoyed by the majors. Our energy exposure is indirect, primarily through North American Construction Group and, to a lesser extent, Velan. We do not expect to outperform in periods driven by oil and gas prices, and we remain underweight this segment of the market.

The quarter was otherwise busy. We added two new companies, exited a long-held position, and made adjustments across several existing holdings. The dominant story — and the most frustrating — was goeasy.

We sold goeasy in March after the company announced write-downs within its LendCare loan portfolio. It was a poor outcome for a position we have held, in various forms, for nearly a decade. The financial loss is one thing. The deliberate deception is another. Management and the board withheld material information about the health of the loan book, allowing investors to operate on a false premise. Restructuring, board changes, and litigation are underway, but we suspect the accountability will fall well short of what is warranted. All board members, including chairman David Ingram, should resign.

We own the error. goeasy was our smallest position when the news broke, but size does not excuse the lapse. A short report had raised serious red flags. We chose to rely on our own decade-long familiarity with the company rather than weigh that signal more seriously. That was a mistake. We will apply greater scepticism to the areas of reporting where management exercises discretion — unaudited metrics, qualitative disclosures, guidance. And we will stay humble about what remains unknowable: some people are simply willing to deceive, and determined fraudsters are difficult to detect in advance.

The most notable addition this quarter was Zedcor, initiated in January. Zedcor deploys mobile surveillance towers to industrial and commercial customers across North America, operating on a rental model that generates recurring revenue. We first encountered the company a few years ago, when its projections seemed overreaching and its management overconfident. We liked the business model but put Zedcor on the watchlist rather than the buy list.

What followed was a prolonged exercise in patience. Quarter after quarter, Zedcor beat expectations. The stock climbed. We watched.

Then, in January, a two-day, 25% selloff gave us our entry point. The catalyst was a rumour that Ring, Amazon’s consumer doorbell camera brand, planned to launch a competing product. We moved quickly to assess the threat. Ring serves homeowners and was promoting a new product that could be used by small businesses; Zedcor serves larger industrial and commercial sites with a fully managed, enterprise-grade solution — the two are not genuinely comparable, and we found no evidence that Amazon was pursuing this market in any meaningful way. The market’s reaction was indiscriminate. Ours was not.

This is the watchlist working as intended: patient observation, followed by decisive action when the moment arrives.

Zedcor’s competitive edge lies less in proprietary technology than in service execution. Customers are migrating away from static cameras and human guards toward real-time, managed monitoring — a long-cycle shift that we believe has substantial runway ahead.

In other portfolio changes during the quarter, in January, we trimmed some gold exposure to manage position sizes. In March, we initiated a position in a small healthcare company that we believe is entering a meaningful inflection in its growth trajectory. We are still building the position and will share more detail in a future commentary.

Performance Review

The quarter’s standout performer was Firan Technology Group, up 61%. Strong results, new contract implementations, and plans to expand capacity across both its aerospace and defence segments drove renewed investor confidence in the stock. Even after that run, we continue to see room for further appreciation.

Two gold holdings added to returns: G Mining Ventures gained 18% and Elemental Royalty rose 13%.

On the other side of the ledger, goeasy was the largest detractor despite being the portfolio’s smallest position — a reflection of just how severe the decline was. Shares fell 62% before we exited. The company had concealed material deterioration in its loan book. When the write-downs were announced, the market responded accordingly. Shares fell a further 23% from our exit price by quarter-end and continued lower into Q2 as the full picture came into view.

Magna Mining slipped 22% on a disappointing quarter and a cautious outlook for the McCreedy mine. Velan fell 15% after the controlling Velan family agreed to sell their stake to Birch Hill, a private equity firm, at a meaningful discount to market value. We continue to believe the shares are undervalued.

Feature - BQE Water

BQE Water — Revisiting the Thesis

We first featured BQE Water in our Q3 2024 commentary. Eighteen months on, the company has become a meaningful position in the portfolio — a reflection of our growing conviction in both the business and the people running it. This is not a re-introduction so much as a progress report: what has happened, what has changed, and why we still see a compelling opportunity ahead.

For those who need a brief reminder: BQE Water provides water treatment solutions to the global mining industry. The company designs, builds, and operates water treatment plants on mine sites, earning long-term recurring revenue, with the mining company covering the capital cost of the plant. With over 25 years of operating history, four proprietary technologies, and 30 plants built globally, BQE has established itself as a technical authority in a niche where relationships, expertise, and a track record of performance matter more than scale.

Restating the Thesis

The core thesis has not changed: a capital-light business model, recurring revenue with strong margins, a durable competitive moat, and a management team focused on doubling revenue over three years. What has changed is our confidence. When we first wrote about BQE Water, much of the upside was prospective — a pipeline of projects we believed would convert. Since then, that pipeline has begun to convert in a meaningful way, and the company has added capabilities and contracts that were not in the picture eighteen months ago.

Tracking the Thesis

We track the progress in operations revenue as a key driver because we believe growing recurring revenue is the most valuable part of the business. It provides a foundation to build upon each year. These contracts are generally stable, easier to predict, and can last decades. As operations revenue grows, it will become a bigger portion of the overall business, and we believe will drive a higher valuation for the business.

The headline numbers for operational revenue in 2025 require some explanation. Operations revenue declined from $10.5 million in 2024 to $7.3 million — a drop of roughly 30% that we flagged internally and examined carefully before drawing any conclusions.

The decline had two specific causes. One larger contract was reduced in scope from full operations support to a supervisory model, reducing the associated revenue. Management agreed to renegotiate the contract, moving from an operating role to a supervisory one. The revised scope has reduced revenue but preserves similar margins. BQE decided to take the long view, believing that once the mine begins production in three to four years, the operator’s need for more support may grow, particularly as the water management process becomes more complex. Maintaining a presence onsite and keeping an amicable relationship was also a factor. This is a base metals mine and once in production could run for 30+ years.

The other factor that contributed to the lower operational revenue was the Minto Mine contract coming to an end during 2024.

Neither reflected competitive displacement or a failure of BQE’s technology — both were site-specific circumstances rather than any erosion of the company’s position or client relationships.

What made us comfortable looking past the operational decline was what was happening on the other side of the ledger. Technical services revenue grew over 300% in the same period, including short-term operational contracts at the Eagle Mine. Technical services work is not just consulting revenue — it is the front door to future operational contracts, and another key metric that we track. BQE’s track record shows that technical engagement converts to long-term operational revenue as projects advance. A surge in that activity, even as one or two operational contracts stepped back, tells us the funnel is filling, not emptying. We chose to look through the short-term revenue mix and focus on what the pipeline was signalling.

How the Company Has Evolved

Several developments since our original feature have strengthened the investment case.

Aquatic Toxicology. BQE acquired an aquatic toxicology team, adding a new service line that engages clients earlier in the mine assessment and permitting process. This matters because it widens the funnel — BQE is now building relationships and demonstrating expertise before they would normally be in the conversation. It also deepens the company’s ability to serve as a single point of technical accountability for mining companies navigating complex environmental requirements.

Building the Team. Management has been deliberate about adding experienced leaders in areas like talent management to support the next leg of growth. In a business where the limiting factor on growth is the pace at which new plants can be commissioned and operated, having the right people in place is not a support function — it is the growth function.

Experience at Eagle Mine. BQE Water’s emergency response at Eagle Mine showed the industry, First Nations partners and government regulators what BQE is capable of. It is now an industry reference case, one that demonstrates BQE Water’s ability to design and operationalize solutions under pressure. BQE Water continues to work onsite today, but we also believe that there is a high probability that they will be there for the long-term. As Eagle Mine makes its way through receivership and into the hands of its new owners, water management will continue to be a critical part of the process. BQE Water has also completed the preliminary design work for the new permanent water plant, further entrenching its position on site.

Longer-term Contracts. The most significant recent milestone is the award of a 20-year operational contract with the BC government for the water treatment plant at the Britannia Mine site. A two-decade contract with a government counterparty is an exceptional demonstration of the recurring, durable nature of BQE’s operational model. It also demonstrates something else – BQE Water can win contracts on water plants that are already in operation. In the case of the Britannia water treatment plant, they displaced an incumbent, a leading multinational, by identifying efficiencies that deliver savings over the long term. More recently, BQE Water announced it had signed a 3-year operating agreement with Canadian Royalties to run five seasonal water treatment systems in Quebec – again displacing an incumbent.

Pipeline. The pipeline of opportunities remains the broadest it has been. There is a greater sense of urgency in the industry. Western countries are looking to secure access to critical minerals. Gold developers want to move quickly while gold prices are high, and the financing window is open. BQE’s pipeline includes a dozen SART and cyanide destruction projects at various stages. Management recently reported active discussions on four other Canadian sites for operations service agreements in 2026. The pace of activity has changed dramatically since we first started our research a few years ago.

Valuation — The Asymmetry

BQE Water’s shares have appreciated meaningfully (~50%) since our original feature, and at approximately $80 per share, the company now trades at a market capitalisation of just over $100 million. With roughly $19 million in cash on the balance sheet and minimal debt, the implied enterprise value is approximately $85 million — that’s approximately 10x trailing 12-months adjusted EBITDA or about 8x our 2026 adjusted EBITDA estimate.

We think the fair value range is 10-12x adjusted EV/EBITDA, informed by comparable engineering companies that are larger and more diversified but carry less recurring revenue, lower margins and a slower growth profile.

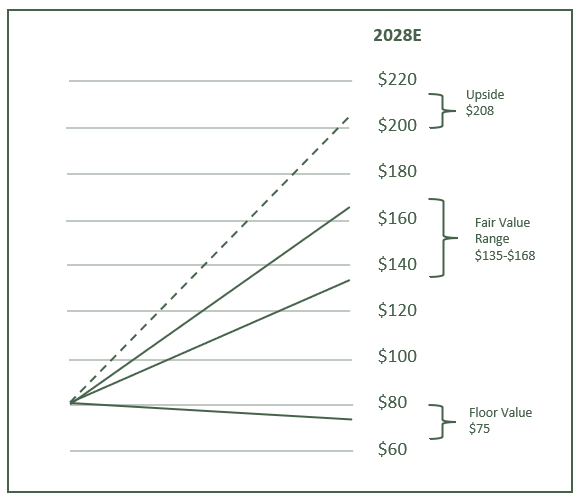

Management has set a clear objective: double the business by 2028. That would require >25% growth for three consecutive years. Our estimates are lower than this as we are trying to be conservative. The chart below shows our fair value range.

We typically look out 2 years in this exercise; here we extend to 2028 because management has set explicit targets.

Our upside scenario assumes management reaches its goal of doubling revenue by 2028 and gains operating leverage, with adjusted EBITDA margins expanding to 25% and resulting in EBITDA of $20 million. Applying a 12x multiple, that implies a share price of $208. We consider these assumptions aggressive, but they are illustrative of a full doubling scenario.

The top end of our fair value range assumes that management reaches $16 million in adjusted EBITDA, just short of doubling, at a 12x multiple, implying $168 per share. The lower end of the fair value range assumes they get to $15 million in adjusted EBITDA and 10x multiple, implying $135 per share. The implied adjusted EBITDA CAGR over the three-year period is 22%-25%. For context, BQE Water grew adjusted EBITDA at a 30% CAGR between 2019 and 2025.

The downside, in our view, is meaningfully cushioned. If BQE Water achieves only high-single-digit adjusted EBITDA growth, reaching $10.5 million in 2028, a 7x multiple implies approximately $75 per share – with roughly 25% of that value represented by cash.

Optionality

Company Maker Projects. In our previous feature we highlighted that ‘company maker’ projects could dramatically change the trajectory of the company, and they still can. We put less emphasis on this today; the timing and probability of these large projects coming online are genuinely difficult to estimate. We continue to monitor several that remain in development, and consider any progress purely as option value.

Capital Allocation. The company is now sitting on $19M in cash and it doesn’t require capital to grow. We believe that if the company can execute on acquiring a small disciplined engineering firm, it could move the needle in several ways. BQE Water would be able to capture more of the construction-phase work that it currently shares with partners and it would capture more value and increase the scope of the technical services team. An acquisition like this could cost between $10-25 million depending on the size and profitability of the firm – but it could add $2-4M in adjusted EBITDA.

BQE Water could also buy back their shares or initiate a dividend given they don’t need the capital to grow and they have a base of recurring revenue.

Take-Out Target. As we highlighted in our last write-up, we believe that BQE Water could become a target as it continues to grow. The company will begin to be on the radar of larger firms now that they have crossed the $100 million market cap level and are nearing $10 million in adjusted EBITDA. We think a strategic buyer might want to add BQE Water’s expertise to their roster at this point in the cycle, given BQE Water’s higher-than-industry-margins and growth rates. We think a strategic buyer could pay a hefty near-term multiple for the company and still make it accretive.

Summary

BQE Water is a growing company with a durable competitive advantage, a strong balance sheet, and a management team executing against a clear and credible plan. The business generates high-quality recurring revenue in an industry where expertise and trust are difficult to replicate. The model is capital-light, the balance sheet is clean, and the pipeline of operational and technical work is the broadest it has been.

We are realistic about the pace of development — mining projects take time, and plants take time to commission. But we are seeing the thesis develop: in contracts won, in capabilities added, and in the growing recognition within the mining industry that BQE Water occupies a category of its own.

The company comes with plenty of optionality. Potential company-maker projects remain in the pipeline. And the balance sheet, at its strongest point in the company’s history, gives management the flexibility to act if the right opportunity presents itself.

We do not need any of that optionality to make the investment case. But we like having it.

Forterra Investment Management Inc. is registered as a portfolio manager with the Ontario Securities Commission and the British Columbia Securities Commission. This commentary is for information only. It is general in nature, reflects the author's views as of the date of publication, and is not investment, financial, legal, or tax advice, nor a recommendation or solicitation to buy or sell any security. Any companies or securities mentioned are used to illustrate the author's thinking, and Forterra and the accounts it manages may hold positions in them, which can change without notice. Investing involves risk, including the possible loss of capital, and past performance does not guarantee future results. Full disclosures are available on the About page.